Africa’s Refining Moment: How the Iran War Is Redirecting Global Energy Investment to the Continent

The disruption of Middle Eastern oil supply is the biggest structural shift in global energy since the 1970s. For Africa’s oil-exporting nations, it may also be the biggest FDI opportunity in a generation.

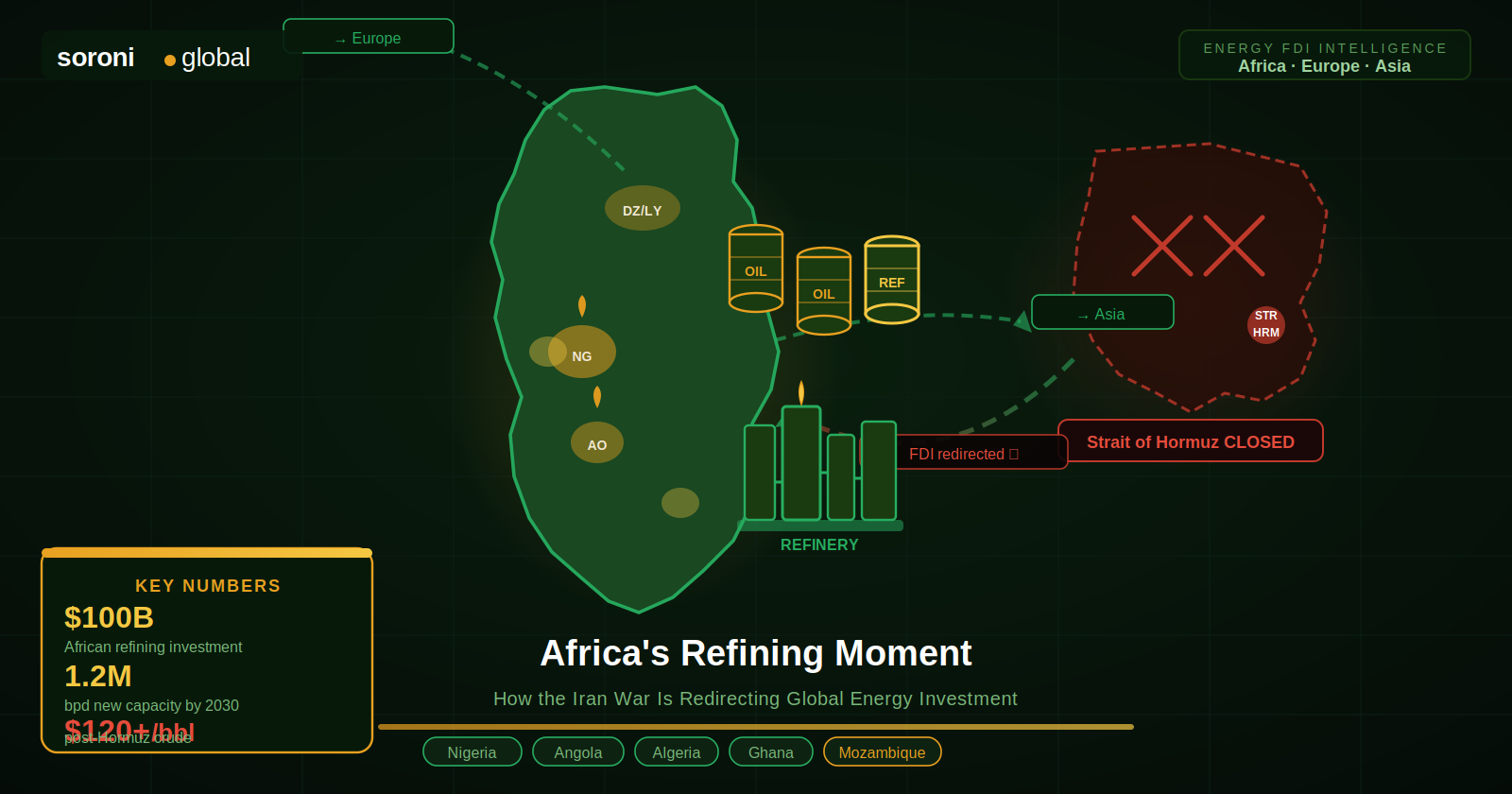

When Iranian forces closed the Strait of Hormuz on 4 March 2026, the consequences were immediate and severe. Brent crude surged past $120 per barrel, triggering what the International Energy Agency characterised as “the largest supply disruption in the history of the global oil market.” Roughly 20 million barrels per day of crude oil and oil products had moved through the strait in 2025, as had roughly one-fifth of global liquefied natural gas trade.

The shock reverberated far beyond oil prices. Saudi Arabia and the UAE, which by 2026 were among the top ten global destinations for FDI — a position neither held a decade earlier — suddenly found themselves operating in a conflict zone. As one senior American political scientist bluntly put it at an investment conference: “We know capital is a coward; it doesn’t go into war zones. And to the extent that tourists, investors, businesspeople see the Gulf as a war zone, they’ve got other places they can invest.”

That observation contains within it one of the most significant economic opportunities Africa has seen in decades. Those “other places” should — and increasingly do — include the continent’s oil-exporting nations.

The Gulf’s Loss Is Africa’s Gain

The flight of investment capital from the Gulf is not speculation. It is already measurable. Saudi Arabia’s FDI momentum, which had only just regained some traction in early 2025 after years of Vision 2030 reform efforts, has been knocked back by the conflict. Analysts warn that discretionary greenfield investment — where firms have the flexibility to delay or redirect — is the most vulnerable category and where near-term slowdowns will show up first.

The Saudi Public Investment Fund, valued at $925 billion, has already signalled a strategic reorientation, with its governor announcing plans to cut international investments from 30 percent to 20 percent of the total. Sovereign wealth flows that once headed to global markets are being redirected inward — meaning the Gulf’s capacity to serve as both an energy supplier and a capital exporter to the rest of the world has simultaneously contracted.

Africa sits in almost the exact opposite position. While Middle Eastern export infrastructure is disrupted and investor confidence in the Gulf wavers, African oil producers — Nigeria, Angola, Libya, Algeria, and Ghana, as well as emerging gas powerhouses like Mozambique — possess vast, under-integrated reserves. Unlike Middle Eastern exports, much of Africa’s oil and gas is Atlantic-facing, allowing it to reach European and American markets without passing through the most vulnerable maritime chokepoints.

This is not a marginal advantage. It is a structural one.

The Refining Gap: Africa’s Most Investable Infrastructure Story

For decades, Africa has suffered from one of the most paradoxical features of its energy economy: the continent exports millions of barrels of crude to Europe, Asia and the Americas while remaining heavily reliant on imported refined products. Limited refining capacity forces many countries to export low-value crude while importing high-value petroleum products.

That equation is now changing — and changing fast. Africa is set to add 1.2 million barrels per day of new refining capacity by 2030, marking one of the fastest downstream expansions globally, according to the 2025 OPEC World Oil Outlook.

The anchor of this transformation is Nigeria’s Dangote Refinery. The Dangote Refinery increased production and supply in response to the surge in global demand, making Nigeria a net fuel exporter of refined petroleum as of March 2026 — including the much-needed aviation and jet fuel now in high global demand, supplied to West African countries and to Europe. Plans are now underway to more than double its capacity. Aliko Dangote has announced intentions to expand the refinery to 1.4 million barrels per day — which, when completed, would surpass India’s Jamnagar refinery as the largest refinery ever built at a single site.

Nigeria is not acting alone. Angola is pushing to bring online the 200,000 bpd Lobito Refinery and 100,000 bpd Soyo Refinery by 2030. Uganda’s refining ambitions are taking shape with a 60,000 bpd facility in Hoima, part of the broader Lake Albert basin development plan. In North Africa, Algeria, Libya and Egypt are all advancing projects aimed at capturing higher margins and reducing dependency on imports.

In Angola, the $470 million Cabinda refinery has already begun supplying domestic and foreign markets. Owned primarily by UK-based Gemcorp Capital, it has a current capacity of 30,000 bpd with plans to double by end of 2026. And Dangote is already looking east: his planned refinery in Kenya, if completed, could reduce East Africa’s reliance on the Middle East significantly.

OPEC estimates Africa will need over $40 billion in refining investments by 2030 to meet its mid-decade objectives — with a further $60 billion-plus required for construction, modernisation and secondary processing capacity upgrades beyond 2030. This opens a $100 billion investment window for project developers, institutional investors and sovereign wealth funds.

The FDI Opportunity: Who Should Be Investing and Why

The case for directing European, Asian, and intra-African FDI toward African energy infrastructure is now stronger than at any point in the continent’s post-independence history. It rests on four converging arguments.

1. Supply security has become the dominant investment thesis.

The IEA’s Executive Director has described the combined impacts of the Hormuz disruption as “the greatest threat to global energy security in history.” European governments and energy companies that once treated Middle Eastern supply as reliable and Gulf investment as lucrative are now urgently reassessing both. Atlantic-facing African supply chains — anchored in Nigerian, Angolan, Algerian and Mozambican production — offer a route to diversification that does not depend on contested waterways.

2. The economics have improved dramatically.

African refining capacity expansion is attracting $100 billion in investment as momentum shifts from crude export toward local production and value capture. African Energy Chamber Executive Chairman NJ Ayuk has been explicit: “Refine, baby refine.” Investors face clear signals — African refining capacity expansion promises returns, policies are improving, and firms like Dangote have proved that scale works.

3. The regulatory and policy environment is improving.

Investment promotion agencies across Nigeria, Angola, Ghana, Senegal and Mozambique have moved to streamline licensing, improve fiscal frameworks and create dedicated energy investment zones. For Economic Development Organisations and Investment Promotion Agencies working to position their jurisdictions as credible destinations, the Hormuz crisis has handed them a powerful, externally validated narrative: African energy is not a frontier risk — it is a strategic necessity.

4. The demand base is enormous and growing.

Over 600 million Africans lack electricity. Some 900 million have no clean cooking solutions. African oil demand is projected to hit 4.5 million barrels per day by 2050. Refining investment serves both export markets and a vast, underserved domestic one.

What African Governments and Investment Promotion Agencies Must Do Now

The opportunity is real. Capitalising on it requires deliberate action from governments, state oil companies, and the Investment Promotion Agencies tasked with attracting the capital needed to move it forward.

Develop investor-ready project pipelines. Capital is available, but it flows to bankable projects. Governments must work with development finance institutions — including the African Development Bank, the IFC and the US DFC — to structure refinery and pipeline projects that meet international investment standards. Vague upstream concessions will not be enough.

Tell the supply security story loudly and clearly. European energy ministries, Asian national oil companies and US strategic investors are actively looking for Middle East alternatives. African IPAs should be presenting at global energy investment forums, engaging European trade missions and briefing Asian sovereign wealth funds on the strategic logic of African energy FDI — not just its commercial returns.

Build regional integration into the pitch. A refinery in Nigeria that can supply West Africa. A Kenyan facility that serves East African landlocked markets. An Algerian LNG terminal that feeds Southern European demand. The pitch to global investors is strongest when it connects upstream capacity to downstream demand through credible regional trade frameworks.

Leverage the AfCFTA energy provisions. The African Continental Free Trade Area creates the legal architecture for intra-African energy trade. Governments that move quickly to harmonise energy trade rules and reduce intra-African tariff barriers will attract more investment than those that treat their refining assets as national monopolies.

The Window Will Not Stay Open Indefinitely

Crises create windows. The Hormuz disruption has opened one for Africa that may not remain open in its current form. Analysts expect the oil market to eventually adapt even in scenarios of prolonged Hormuz disruption, with prices consolidating as new supply routes and sources are established. The countries and companies that act decisively in this window — building refining capacity, securing FDI commitments, and embedding themselves into new global energy supply chains — will hold structural advantages long after the immediate crisis has passed.

Africa’s oil-exporting nations have spent decades supplying the world with raw crude and importing back the refined products it generates. The Iran war has, paradoxically, created the conditions for that equation to finally reverse. The question is not whether the investment opportunity exists. It clearly does. The question is whether African governments, their investment promotion agencies, and their private sector partners will move with the urgency the moment demands.

Explore more from SoroniGlobal:

- 2026 Investment Attraction Strategies — How EDOs and IPAs can position themselves in today’s competitive investment environment

- FDI Attraction & Promotion Services — How SoroniGlobal helps Investment Promotion Agencies attract capital

- FDI Lead Generation — Identify and engage the investors most likely to act on your opportunity

- FDI Consulting Services — Strategy, value proposition development and market positioning for EDOs and IPAs

- How Ghana Can Move Up the Cocoa Value Chain — A related perspective on African value-added industrialisation strategy

SoroniGlobal is a specialist marketing consultancy for Economic Development Organisations, Investment Promotion Agencies and Tourism Promotion Organisations. If your IPA or government agency is looking to position your energy sector as a destination for international FDI in the current environment, get in touch.